This past week, the housing market received a surprising housing report from the National Association of Realtors® (NAR). The news media and online blogger community have been aflame about the disappointing sales numbers that were recently posted for the month of November. While I try to shy away from over-analyzing the data movements on such a scrutinized level, this report is getting so much attention that it is worth explaining in a little more detail so that would-be buyers and sellers can put the headlines into proper perspective.

The Housing Report

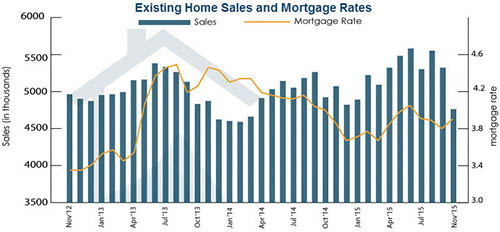

According to the report released by the NAR, November sales of “existing” (ie: pre-owned) homes came in drastically lower than expected. Compared to the prior month’s numbers, analysts were expecting existing home sales to slightly slow based on a normal seasonally-adjusted rate, but even with that modification the numbers were significantly lower than anticipated. Closer to home, the report showed that existing home sales in the Northeast declined 9.2 percent to an annual rate of 690,000, while the median price in the Northeast was lower than anticipated at $254,800.

Additionally, first-time buyers accounted for 30 percent of all home buyers in November, while the first-time buyers segment typically had been accounting for close to 40 percent of activity. Home prices are rising faster than wages, which presents a major obstacle for potential home buyers. Furthermore, “all cash” buyers made up 27 percent of all transactions, which is down considerably from previous accounts.

The Melodramatic Reaction

Part of the reason this report is getting so much attention is because the housing market has consistently been providing a substantial boost to the U.S. economic growth over the past few years. A growing labor market and low interest rates have helped many home buyers take action, and has continually resulted in increased housing sales—and thereby a stronger housing market. As my father always says, when homes are selling the entire economy benefits. Aside from the obvious benefit to Realtors, lenders, attorneys and the like, goes beyond that to contractors, movers, builders, painters, plumbers, electricians, home-improvement businesses, etc. – the list goes on and on.

Coming on the heels of the historical Federal Reserve rate increase, however, this surprising and disappointing report is ripe for severe scrutiny. Some are seeing the sharp decline as a potential warning sign for the overall health of the U.S. economy. Others say the economy is strong enough even if housing were to slow down from its past few year run. Typically, such a significant drop in sales is unusual except in cases where certain housing tax incentives or housing credits expire and cause home sales to drop after a last minute increase in home purchases by home buyers rushing to take advantage before a deadline. Several notable analysts referred to it as a “statistical anomaly.”

Behind The Headlines

The NAR chief economist, Lawrence Yun, said that multiple factors may have contributed to November’s sales decline. The primary reason could be an abnormality as the industry adjusts to the new CFPB “Know Before You Owe” mortgage regulations. It is likely that these new “TRID” regulations (previously discussed so eloquently in the Jewish Link by Carl Guzman) may have increased the closing period for many home sales, and delayed closings into December that otherwise could have closed in November. In addition, “Sparse inventory and affordability issues continue to impede a large pool of buyers’ ability to buy, which is holding back sales,” Yun said.

There are other housing reports that surfaced that were not all negative. For example, the FHFA Home Price Index, which measures prices on single family homes, showed that home prices increased by 6.1% since last year. To quantify just how meaningful the 6.1% increase can be — if you bought a home for $450,000 last year, that same home would be worth $477,450 this year. That is a $27,450 gain in appreciation!

Moreover, signed contracts have remained steady in recent months, and properties are selling at a quicker pace that usual based on the November report. There was a 5.1 month supply of existing homes for sale in November, while the average supply has typically been six months. All in all, there is nothing to panic about. It is highly possible the decline was not because of sudden or declining housing demand and that the temporary lull will snap back next month for the December statistics. We will have to wait and see before passing judgement.

For home buyers and sellers, while the headlines can give you pause, it should be business as usual, and everyone who is serious about making a move should rigorously take advantage of the winter sales months. As always, dealing with a competent and knowledgeable real estate or finance expert will give you the best advantage and insight in making the right decisions in this market and beyond.

Shmuel Shayowitz (NMLS#19871) is President and Chief Lending Officer at Approved Funding, a privately held local mortgage banker and direct lender. Approved Funding is a mortgage company offering competitive interest rates as well specialty niche programs on all types of Residential and Commercial properties. Shmuel has over 20 years of industry experience including licenses and certifications as certified mortgage underwriter, residential review appraiser, licensed real estate agent, and direct FHA specialized underwriter. He can be reached via email at [email protected]

By Shmuel Shayowitz