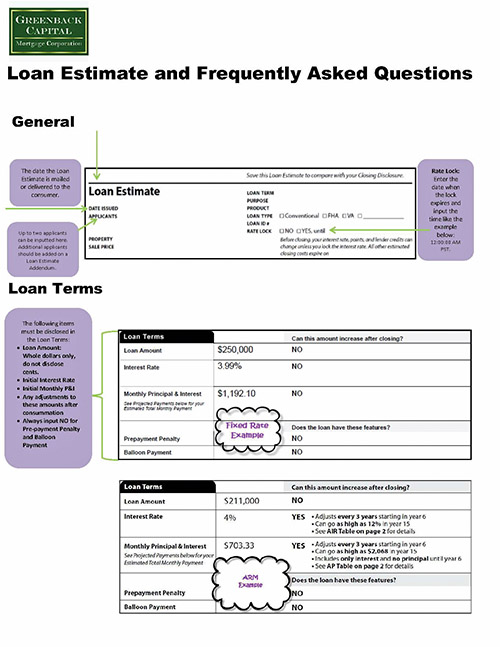

The first question you may have is: what is a loan estimate (LE)? If you bought or refinanced a residential one- to four-family property in the past two years and obtained financing, then you know that it’s the initial estimate of closing costs and summary of your transaction. If the last time you bought or refinanced a property was over three years ago or more, then you are familiar with the good faith estimate (GFE) and truth-in-lending disclosure (TIL). If you are embarking on the journey to homeownership for the first time, you’ll appreciate the introduction to a very important disclosure that needs to be reviewed with care. The bottom line is that our government decided to nix the GFE and TIL and combine them into one form called the LE. The LE is required to be issued within three days of a borrower applying for a loan. They also increased the liability of lenders and mortgage brokers in terms of the accuracy of their LE (so the LE better be pretty much on target and yea for the consumer). There are closing costs that have a “zero tolerance,” meaning that if they are under-estimated, too bad on the lender—they have to eat the cost difference. There are other costs that have a 10 percent cumulative tolerance that allows for an estimate on these costs to be 10 percent off the initial estimate, with certain caveats.

As they say in the boy scouts, “be prepared,” so the LE infographic below (I think it’s an infographic, anyway) should help you out when you start shopping for your mortgage. If you currently have a loan estimate, put it side by side and see if it clarifies your LE for you. Feel free to email me with any questions you may have. Read on…

By Carl Guzman