It’s predicted that over the next two months, inflation is going to come down further, which usually translates into lower mortgage rates. Lower mortgage rates typically trigger a push for buyers to enter into the housing market, thereby driving real estate prices up, especially in a tight inventory environment. The natural question then becomes, how much will rates come down? It may depend on how much inflation will come down. That being said, factor the respective prediction of lower rates into your current financing decision, but make the best decision for now because who can predict the future?

If you are looking for additional cash, the question is how do you go about getting it? Assuming you don’t have a trust account or relatives that will give or lend you the money, that leaves the following:

Credit cards: Unsecured, but high interest.

Savings: But do you want to deplete your savings or investments accounts?

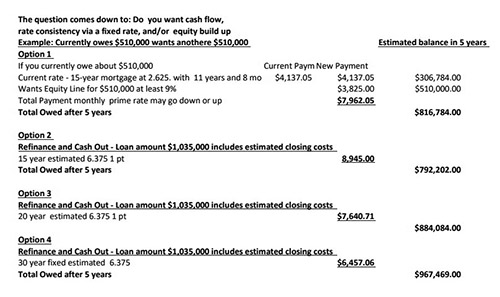

Mortgages cash out or second mortgage equity lines. Do you want improved cash flow or equity buildup? See analyses below.

Other mortgage products: Ideas below.

Other Mortgage Financing Ideas for Debt Consolidation, Cash Flow Help and Equity Acceleration Options:

First mortgage equity lines with a checking sweep account. The chances are you’d benefit greatly from this product, if you live within your means and earn or have a vehicle for earning predictable consistent cash flow.

A cash flow analysis is important to see if you can benefit, but, if your situation fits, this mortgage can cut paying down the mortgage by at least 10 years, and still give you the flexibility of being able to tap the equity in your home. The overall cost of the mortgage is reduced substantially over time. Once you understand the concept of “rate doesn’t matter, but it’s the cost over time,” you’ll appreciate the benefits of this mortgage. The sweep-account structure allows you to direct your salary/bonus/additional income/savings to pay into the mortgage immediately, thereby reducing your interest rate costs monthly, annually and collectively. The product design, correctly structured, will accelerate the reduction of the loan balance and the total cost of the mortgage while still keeping access to your money liquid.

Other reasons to consider refinancing are as follows:

1. Damaged credit may have improved. Improved credit scores open the door to possibly refinancing at a rate better than an existing rate.

2. Credit card debt can be super-expensive as well as student debt. Number crunch and see if a new loan can improve your cash flow. (Forget about the rate itself).

3. It may be that you have paid your 30-year, fixed-rate down enough to switch to a 15-year fixed rate, even at a higher rate, and knock off your existing loan in 15 years.

4. Pay off an existing mortgage with a reverse mortgage and free up cash (great product for the right people over 58 years old).

5. Fixed rates are up, but an alternative and great solution may be to explore adjustable rate mortgage products. Most don’t adjust for five, seven or 10 years and can make sense for homeowners with lots of equity if they plan to downsize or pay off the loan within that respective time frame.

6. Eliminate existing mortgage payments. The reverse mortgage can be used to pay off an existing “forward” mortgage to create additional cash flow and also strategically as a tax-free income source to defer taking Social Security, so you can get the maximum Social Security payment at 67. For those with stock portfolios that have appreciated, look at where the market is now. If you’re 60 or older and do not want to be forced to liquidate your portfolio, I would suggest looking at a reverse mortgage as a viable option and tool.

7. A balloon mortgage coming due—long-term loans having minimal or no amortization of the outstanding principal, and a due date (payoff date) earlier than the term are called balloon loans (or interest-only loans). The loan principal is not self-amortizing; therefore, a lump sum principal payment is due at a point in time specified in the mortgage note agreement, or the outstanding principal balance will amortize over 20 years at a substantially larger payment.

8. Refinance out of an unconventional mortgage. Maybe when you bought your home, you could not qualify for a standard mortgage. The reasons vary, but sometimes a self-employed borrower may not have the income or documentation that would qualify them for a standard mortgage. Things change as time rolls on.

When you’re self-employed, depending on your business structure, the usual setup, in terms of income distribution, is to usually give yourself a salary, and distribute any extra profit (either as a partner or LLC or sub-S). Then you have the discretionary “perks” such as health insurance, car leases, travel and entertainment, credit card payments and other personal/business items. You must have in mind that mortgage lenders look at consistency; typically two years is the standard, bar any program exceptions and special underwriting overlays. If you have paid yourself as a w-2 previously, you maintain that history, but if you become a consultant paid on a 1099, you have set your clock back two years because lenders want to see a two-year self-employment history. If your income was low in the previous year, take less expenses for the upcoming tax year; if practically possible, beef up your income, pay the tax, and get the benefit of a better mortgage rate. Structure salary enough to qualify you for the mortgage financing you may be looking for down the line. Don’t change the business structure until you close on the loan!

Remember, for any mortgage financing low credit scores cost big bucks. Work on increasing your scores to get the most favorable mortgage deal.

Carl Guzman, NMLS# 65291, CPA, is the founder and president of Greenback Capital Mortgage Corp. and www.Mortgagegenius.com. He is a real estate mortgage banker and business financing expert with over 33 years’ experience. He currently has 214 5-star reviews on Zillow. Carl and his team will help you get the best mortgage financing for your situation, and his advice will save you thousands. www.greenbackcapital.com [email protected]