We are nearing the end of the summer. It has certainly been eventful for us here at Julius Wealth Advisors, the markets at large, and me personally. I am currently on my first-ever visit to Israel. Enjoying our Promised Land for the first time with my family is a huge milestone. Just like any milestone, this is the perfect time to assess progress made so far and refocus on how to move forward.

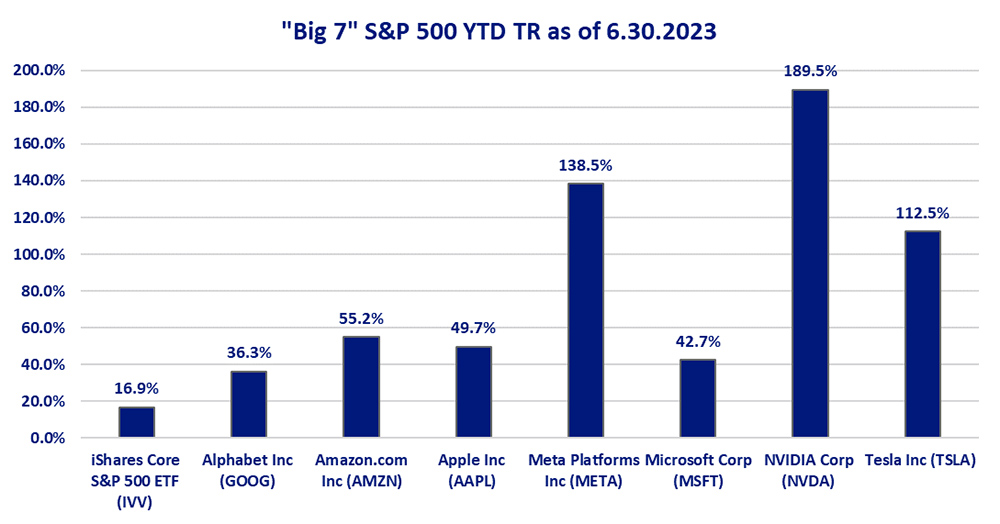

On the topic of progress, let’s discuss the market. The global market, as measured by MSCI All Country World Index (ACWI), has been rallying up ~+26% off the lows hit Oct. 12, 2022 till the end of Q2 2023. Additionally, the S&P 500 and MSCI ACWI are up 16.9% and 14.2% respectively through Q2 2023.

Upon reading this, you’d be forgiven for thinking this means that all businesses are doing well; however, this is not the case. The market in totality hasn’t rallied as a whole. ~74% of the gain through Q2 in the S&P 500 has been shouldered by only seven companies1.

And now these seven companies make up about 27.7% of the S&P 500, while just five and 10 years ago, the top seven holdings only represented only 16.8% and 13.7%, respectively— 1 displaying both the absolute size and relative concentration of these seven companies!

The irony of this, which I unfortunately saw often as Big Tech started to bottom out, were the headlines that shouted “the end is near” and that people should get out of big tech.2 Today, it’s the strength of large-cap, big tech that is holding up the market so far this year.

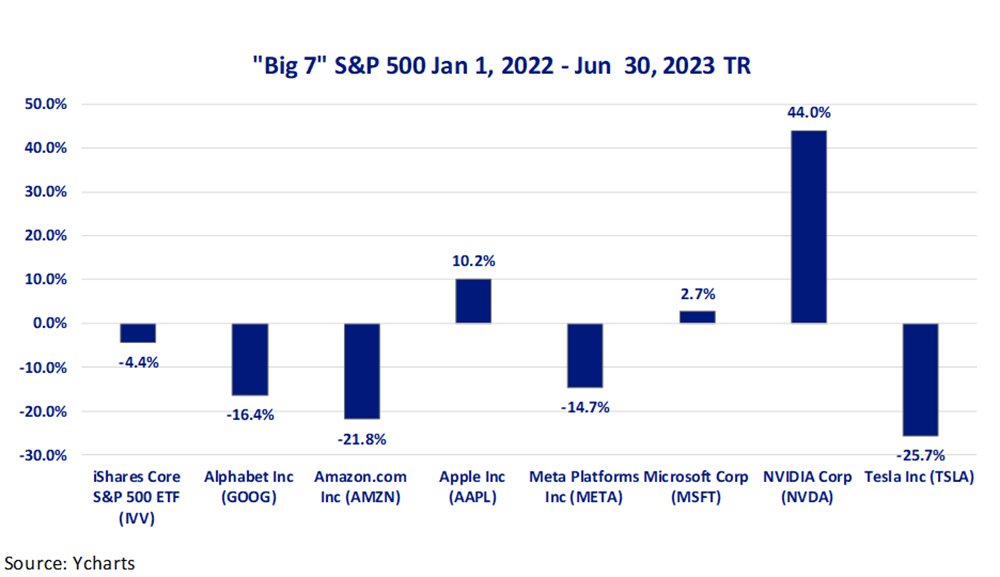

However, just taking a small step back to the beginning of the market downturn in January 2022, you can see that only three of the “Big 7” are positive and have outperformed the S&P 500 (Apple, Microsoft, and NVIDIA). A gentle reminder to not get caught up in extreme shortsightedness.

On the other hand, small-cap companies are underperforming with the MSCI All Country World Small Cap index up only 8.3% through Q2 2023, and still down -11.5% since the start of 2022.

So, to say that the market is rallying would be like assessing the performance of a football team based on a handful of players. The Miami Dolphins may have Tyreek Hill and Jaylen Waddle catching passes, but if the others neglect their roles (let’s go Tua and the offensive line!), no one brings home the trophy.

The Big Apple and Mister Softee

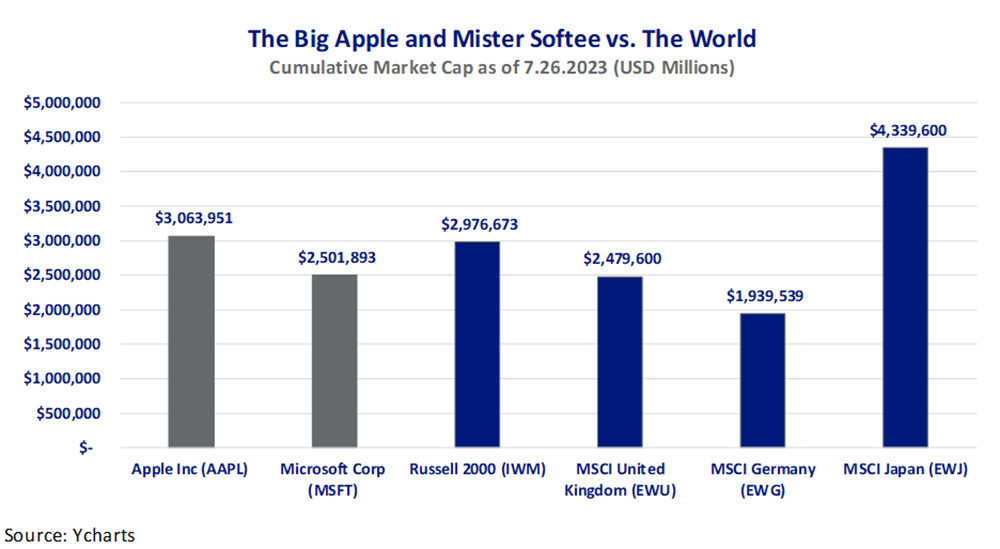

Speaking of big tech, Apple has become the first company in history to hit a $3 trillion market cap, with Microsoft not very far behind at about $2.5 trillion. While these are remarkable accomplishments, when I see this it makes me want to dig deeper to see if this makes logical sense. So, let’s compare:

The equity value of Apple and Microsoft are so large that you can:

Buy every single U.S. Small Cap company vs. AAPL and still have about $1B left

Buy every single company in the United Kingdom index (the sixth largest economy) or AAPL/MSFT

Buy every single company in the German index (the fourth largest economy) or AAPL/MSFT

Buy 71% or 58% of the entire Japanese Index (the third largest economy) or AAPL/MSFT

Think about that for a second. Two single companies, founded in a single country, are valued higher than every single public U.S. Small Cap company and the largest public companies in the largest economies in the world!

The more things change, the more things stay the same. Markets and the value of businesses within those markets will differ over time. At times with emotions detaching from fundamental reality. However, one investment philosophy I’ve found to be reliable since the age of 10 is one from the likes of Charlie Munger and Warren Buffett—owning high-quality businesses at fair prices. These are the businesses that usually survive the ebbs and flows of markets with solid long-term results. These businesses are usually the cornerstone of true long-term wealth creation.

Back to Reality

Aside from the warnings against big tech, the other prediction we heard plenty of last year was that a recession was around the corner. Well, so far, we are yet to enter into a recession. As I’ve touched on, the market as a whole certainly hasn’t rallied but many stocks, it appeared, had been priced for a recession. Additionally, monetary policy remains strict. This is evidenced by the M2 money supply (how much money is in the system).

In 2020, during the pandemic, this number skyrocketed and inflation soon followed suit. It peaked in July 2022 but not after rising an astonishing ~42%. However, money supply has been falling for almost a year now, down almost 4% from the peak.

Additionally, the Fed just raised interest rates by another 25 bps to 5.25-5.5%, the highest in 22 years.3 This should further propel restrictive tightening in the economy as this number is now above both CPI at 3% and core CPI (inflation ex. volatile food and energy) at 4.8% in June.

The good news is that CPI and core CPI have come down from their peak of 9% and 6.6%. There is a general hope that interest rates across the board will soon fall accordingly and return to the “ideal years” of zero interest rate policy. Which is somewhat comical to me when you put this idea into perspective.

You see, in 2007 I bought my first apartment. When I did, the interest rate on my 30-year mortgage was 6.5%. When I shared this with people, they congratulated me and said, “Wow, that is a great rate!” Fast forward to today, where mortgage rates are roughly at the same level. And now the general response is, “Oh no, that’s horrible!”

Over 16 years later, the same number has received a very different reception! This is because people have become addicted to the incredibly low interest policy of the past. A serious amount of steam would need to be sucked out of the global economy for the effects to be felt in a meaningful way. Due to a number of factors, which I’ve discussed in prior articles, I don’t see interest rates dropping much for the foreseeable future. I believe those waiting for this to happen should pull up a chair and get comfortable.

Valuation of Housing

The subject of interest rates is often brought up in relation to housing. The interest rate at a given time is commonly used as a large factor of whether it’s an affordable time to buy a house. I’ve been hearing a lot more people discussing getting into real estate now by either buying their first home or investing. They want to do this because they’ve seen, heard,and read about the gains that many have obtained through investing in real estate in the past.

The problem is that today’s market isn’t yesterday’s, both interest rates and prices have gone up considerably in recent years while incomes have not followed—which in turn, makes houses less affordable. Case in point, the Federal Reserve Bank of Atlanta’s home affordability monitor4 is at low levels not seen since 2006. In my opinion, real estate probably won’t bring the same returns going forward until these trends reverse.

Unemotionally Moving Forward

Unfortunately, we’ve seen the repetition of familiar patterns this year. More and more people are trying to emotionally shock your ancestral brain to sell fear. Fear of a recession, fear of success in the market and fear of an uncertain future. This may have served our distant ancestors to survive the predators of the wild, but the capital markets usually don’t operate under the same conditions.

My goal, and the goal of Julius Wealth Advisors, is not to sell you anything except a long-term relationship based on integrity, knowledge and passion. One where we are collaboratively knowledgeable of the worst, though passionately hopeful for the long-term future of this world.

Living your life in fear means living your life in the back seat. Fear will often hold you back from achieving your dreams and growing the wealth that you work so hard to generate. Furthermore, you can’t live your life on other people’s terms—otherwise known as going with the herd. Instead, you need to invest in hope, invest in those around you, invest in the things that you’re most passionate about, and invest in yourself. This mentality is what historically pushes the markets forward, it pushes society forward and keeps us on the right track.

With the right integrity, knowledge and passion, you can seek to achieve the life that you’ve dreamt of. I can say this as I have achieved this for myself, and I look to guide every single one of my clients to achieve theirs.

This is the power of hope!

Jason Blumstein, CFA® is the CEO and founder of Julius Wealth Advisors, LLC (www.juliuswealthadvisors.com) a registered investment adviser. He is also the host of “The Big Bo $how” podcast available on Spotify and Apple podcasts. Blumstein has been investing and educating himself on personal finance since the age of 10. His company’s mission is to empower people to live their best financial lives while fostering an ecosystem of integrity, knowledge and passion! Blumstein resides in Englewood with his wife and two kids. He can be reached at (201) 289-9181 and/or [email protected].

Disclosures:

This piece contains general information that is not suitable for everyone and was prepared for informational purposes only. Nothing contained herein should be construed as a solicitation to buy or sell any security or as an offer to provide investment advice. The information contained herein has been obtained from sources believed to be reliable, but the accuracy of the information cannot be guaranteed. Past performance does not guarantee any future results. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. For additional information about Julius Wealth Advisors, including its services and fees, contact or visit adviserinfo.sec.gov.

References:

- Sources: Factset, YCharts, and Grandeur Peak Global Advisors

- Tech stocks have been crushed. What’s next for the FAANGs? (cnn.com)

- Fed approves hike that takes interest rates to highest level in more than 22 years (cnbc.com)

- Federal Reserve Bank of Atlanta-Home Ownership Affordability Monitor (atlantafed.org)