With the market’s sharp declines so far in 2022, it’s almost impossible to have a conversation about investing without the word risk or its close siblings volatility and uncertainty coming up. You’ll hear things like “it’s too risky,” “markets are volatile,” and my personal favorite, “there is uncertainty.” Sound familiar?

These terms are often used with a few breaths of each other, but, in my opinion, are often misused, or at a minimum mischaracterized. So, what exactly is risk in terms of your finances? What is volatility? What is uncertainty? Is the relationship between these words as strenuous as the words suggest?

Let’s dive in. The financial services industry’s measurement of risk is typically standard deviation or dispersion around the mean1, which is generally viewed as a bad thing. When the market or an asset is viewed as volatile, interest typically becomes scarce. After all, we’re told from a young age not to take risks with our money—especially when it comes to the market. The funny thing about volatility/standard deviation/uncertainty is that assets tend to get less volatile before they swing the other way, which gives people a false sense of risk. Don’t believe me? Let’s look at a few examples:

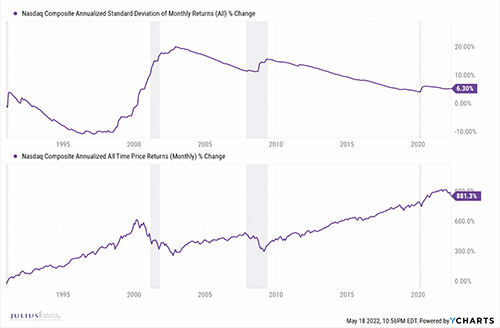

Ex. 1—Late ’90s Tech Bubble

While many younger investors of today weren’t even born, the original #FOMO days were in the late 1990s. While I was only in high school at the time, since I have been investing since the age of 10, I remember these days well. I once made $3,000 (a lot of money for a 16 year old!) in a day when a biotech company I purchased went from $6 a share to $80 on a single day! Funny enough, I told my mom I needed to go to school late the next day so I could sell it at the open. While my investment philosophy has adopted over the years as I get older and attempt to get wiser, the lessons learned do not.

As the chart below demonstrates, the standard deviation, or perceived riskiness of the tech-heavy Nasdaq went down all throughout the ’90s as the returns went up, causing a misplaced sense of lower risk.

Then, when prices start to plummet, volatility spikes from 2000 to about 2004, just to see the returns bottom out, and start to go back up, while perceived riskiness starts to fall all through the recent day.

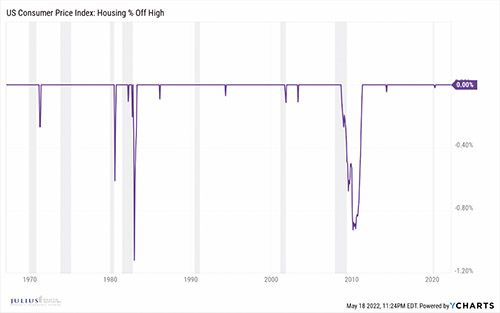

Ex. 2—Housing Market

“Invest in housing; it never goes down!” This was a piece of advice I often heard in the mid-2000s. Well, as the chart below demonstrates, this was a true statement from about the early ’80s through 2008.

Until it was not!

Again, financial markets mispriced risk, thinking housing was a safe, non-volatile asset, all the while creating esoteric financial instruments, leverage and bad lending standards—all based on this backward-looking thought process. Which almost took down the entire banking system!

I vividly recall going into work at J.P. Morgan the day after they announced they would buy Bear Stearns for $2/share2, which had their headquarters right next door. Eerie, heartbreaking feeling, as the typically bustling streets were empty.

Ex. 3—Global Equity Markets

And, to zoom it out to the global markets as a whole, the phenomenon can be seen when looking at global equities as a whole as measured by the MSCI ACWI (All Country World Index).

Standard deviation, or risk goes down as markets climb, just to see the reverse take place … as markets fall, risk goes up.

Pretty much the opposite of what the financial services industry tries to teach people!

Heroes Get Remembered But Legends Never Die

The above examples are pretty much the opposite of what the financial services industry tries to teach people! When assets look less risky, let’s buy them, and when they are more, let’s run away!

This is why the legendary Warren Buffett stated in the 1986 Berkshire Hathaway Shareholder Letter3 the now often-quoted line, “We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.”

The usual wisdom is to hide your money when the market is volatile, and wait till things are not uncertain. Well, when is anything certain in life, outside of death and taxes, as the saying goes!

However, when the market is volatile, as Mr. Buffett noted, this is actually historically when you want to invest. Here at Julius Wealth Advisors, we have long noted this misplaced notion of risk that unfortunately permeates this industry. Thus, we simply believe that risk is the probability of you not being able to build sustainable wealth in the long term.

Why We Look at Risk This Way:

1. No one ever knows what is going to happen in the short term: I was around AIG when it collapsed after all the “geniuses” signed off that it would be OK, without knowing what a financial derivative was. I witnessed even more “geniuses” at major Wall Street firms who are still sitting out of investing post-the 2008 financial crisis, waiting “for more certainty.” During COVID-19, the single biggest day I had of clients vehemently demanding their money back was March 23, 2020, the day markets bottomed out during the pandemic. I ask you, what does the market look like today?

2. There is a lot of confusion over what influences markets: As much as the media tries to make us believe otherwise, there is very little correlation between owning equities in business and the state of the U.S. political system4. The data speaks for itself. Or to put things another way, you’re still going to buy groceries, clothes, and fill up your car regardless of who is sitting in the Oval Office.

3. Choice of Businesses: When you invest in equity markets, you own businesses, not prices on a screen that randomly fluctuate in the short term. If you are scared to own a business for less than a few decades, you shouldn’t have bought it in the first place.

4. Emotions and investing do not mix: This is where our behavioral coaching comes into play. Emotions often spike during periods of stress; thus we attempt to operate as your objective sounding board. Trying to look at the numbers, not emotions.

5. The nature of returns: Your returns are a function of price appreciation, dividends and taxes. Most people forget that last part. When people brag about how much they made on a certain position or cryptocurrency, then sold, did they mention that they had to pay Uncle Sam a hefty percentage of this return5? Notice how they seem to always leave that part out

6. There is no truly risk-free investment: When people ask me what will happen in the market, I openly admit I have no clue what will happen in the short term. What I have witnessed is that it seems like every three to six months there are new issues people worry about. Then as we get through them, in the next three to six months there are new issues that cause people to worry and forget about whatever it was that they were worried about previously. We want to remind everyone, U.S. Treasuries are the only asset that is known to be risk-free6. Everything else comes with uncertainty, and it is this uncertainty that has historically handsomely rewarded investors, not traders!

How to Try to Limit Risk:

There is no way to remove risk entirely. What you can do, however, is limit your exposure to it.

Step 1: Change Your Mindset

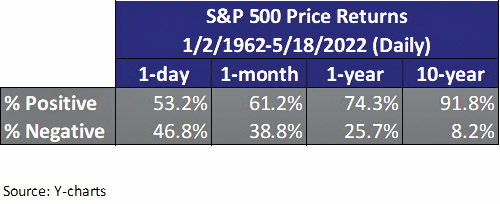

The first thing we believe that you need to understand is that volatility does not always equal risk. Take the S&P 500, for example. If you invested on any random day from the beginning of 1962 through current, and held for a day vs. a month vs. a year vs. 10 years, your probability of a positive return skyrockets!

It goes from a random coin flip of almost 50/50 on a one-day holding period to a 92% probability after holding for 10 years!

Change your mindset to understand volatility and risk separately, so you are able to truly understand what is in front of you. Volatility can potentially be a door to opportunity.

Step 2: Change Your Behavior

Stop chasing the get-rich-quick bandwagon. To do this, we believe you need to remove emotions from your investing behavior. When you check your positions, and see red numbers and dropping arrows, it’s understandable to want to cut your losses and run. Simultaneously, it’s also understandable to want to cash out when you see some great returns. (Don’t forget, Uncle Sam will take his cut.)

It is our belief that when you take emotions out of your decisions, you can start to make better financial choices. Furthermore, you’ll stop listening to the crowd. This will help you to stop falling into the trap of FOMO investing, and instead, make better decisions for yourself.

Step 3: Change Your Selection Criteria

You can’t reach this step until you complete the first and second steps. This step is crucial, and is lifted straight out of the Buffet playbook (widely regarded as one of the best investors of our age). Essentially, your aim should be to only invest in the best possible businesses that aren’t subject to the hype train, and therefore, typically aren’t as risky.

These are businesses with a good return on equity, healthy cash flow, and minimal debt. These are businesses that are positioned to continue operating despite the ebbs and flows of the market, and have a buffer to protect themselves when times are tough.

Unprofitable businesses typically can get mispriced due to hype and people hoping they will one day turn a profit, but they typically get found out. (Please refer to the most recent burst of the tech bubble.)

Understanding Risk

As discussed throughout, we believe the traditional financial industry measurement of risk isn’t always your enemy. In fact, it’s something that you can use to help make better decisions. If you’re uncertain which businesses fit this profile, how to change your behavior, or simply get yourself on track to achieve your financial goals, make the decision to contact us today.

About the Author:

Jason Blumstein, CFA® is the CEO and founder of Julius Wealth Advisors, LLC (www.juliuswealthadvisors.com) a registered investment adviser. He is also the host of “The Big Bo $how” podcast available on Spotify and Apple Podcasts. Jason has been investing and educating himself on personal finance since the age of 10. His company’s mission is to empower people to live their best financial lives, while fostering an ecosystem of integrity, knowledge, and passion! Jason currently resides in Englewood with his wife and two kids. He can be reached at 201-289-9181 and/or [email protected].

Disclosures:

This piece contains general information that is not suitable for everyone and was prepared for informational purposes only. Nothing contained herein should not be construed as a solicitation to buy or sell any security or as an offer to provide investment advice. Past performance does not guarantee any future results. For additional information about Julius Wealth Advisors, including its services and fees, contact us or visit adviserinfo.sec.gov.

References:

1. Standard Deviation, Robertniles.com

2. JP Morgan Agrees to Buy Bear Stearns for $2 a Share, CNBC.com 3/16/2008

3. Berkshire Hathaway 1986 Annual Shareholder Letter

4. We Looked At How The Stock Market Performed Under Every U.S. President Since Truman—And The Results Will Surprise You, Forbes.com 6/23/2020

5. Topic No. 409 Capital Gains and Losses, IRS.gov

6. Risk-Free Asset, Investopedia.com

By Jason Blumstein