If you had to guess, how likely is it that you’d be unable to work for three months or more at some point in your career due to illness or injury? It’s an uncomfortable thought — feel free to skip to the Bahamas travel pages instead.

Most people severely underestimate the risk. In fact, 64% of people believe their chances of experiencing a long-term disability are less than 2%. The reality? The odds are much higher.

The Numbers Don’t Lie

According to the Council for Disability Awareness, a 35-year-old female non-smoker, with a normal BMI who works a desk job and leads a healthy lifestyle, has the following risks over her career:

- 24% chance of being unable to work for three months or longer due to illness or injury.

- 38% chance of disabilities lasting over three months will continue for five years or more.

If a disability lasts longer than three months, the average duration is 6.8 years; this is because some issues are shorter, some last a lifetime.

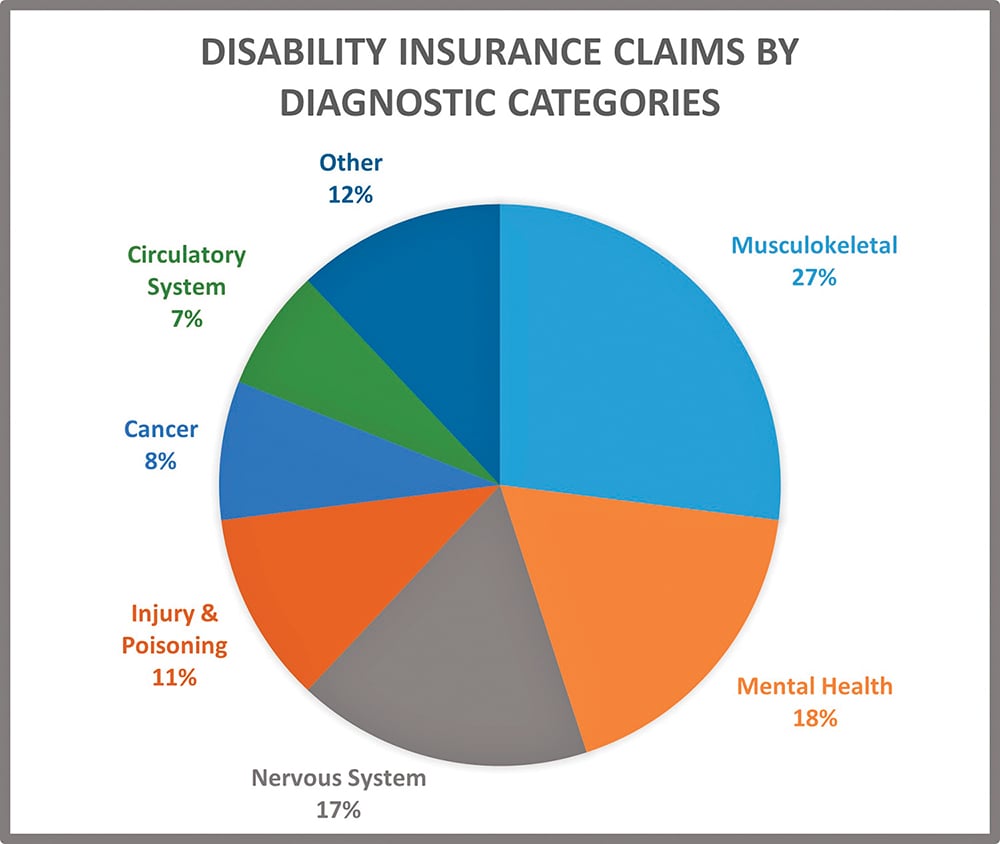

Still think disabilities are rare?

What Actually Causes Disabilities? (Hint: It’s Not Skiing)

When people hear “disability,” they often picture catastrophic accidents: ski wipeouts, car crashes, etc. But in reality, 90% of long-term disabilities are caused by illness, not accidents.

Here are the leading causes of disability claims for individual disability insurance policies with a major U.S. carrier, including a few examples:

- Musculoskeletal disorders (back pain, arthritis, joint problems) – 27%

- Mental health conditions (depression, anxiety, substance abuse) – 18%

- Nervous system disorders (Multiple Sclerosis (MS), Parkinson’s, strokes, seizures, brain tumors) – 17%

- Injury and poisoning (head trauma, toxic substance exposure) – 11%

- Neoplasms (cancer) – 8%

- Circulatory system (heart disease, blood clot disorders) – 7%

- Other – 12%

Many of these conditions don’t happen overnight. They develop gradually — until one day, continuing your job becomes difficult or impossible.

The Financial Fallout

We like to think we’re financially prepared for life’s curveballs, but the numbers tell a different story:

- 68% of Americans would struggle financially if their paycheck were delayed by just one week.

- 65% say they couldn’t cover basic living expenses for a year if they lost their income.

- 62% of personal bankruptcies and 50% of home foreclosures are tied to medical problems.

If losing a single paycheck is a problem, imagine losing income for three years. So what happens when someone without individual disability insurance gets sick or injured? They’re left relying on limited employer benefits, draining their savings or leaning on family. And too often, none of those options are enough.

The Role of Individual Disability Insurance

Here’s the good news: while disability insurance can’t prevent a chronic illness or back injury, it can avoid having financial stress add to a crisis.

Think of it this way: if you had two job offers — one paying $100,000 per year with no safety net, and another paying $97,000 per year but providing income protection until retirement if you got sick or injured — which would you take?

I know my answer (and it’s the one I’ve personally chosen for my own finances). That’s how individual disability insurance works. It pays you to protect the paycheck you depend on, allowing you to focus on recovery instead of scrambling to pay your mortgage.

The Bottom Line

The biggest myth about disability isn’t just that it’s rare. It’s the belief that it won’t happen to us.

The real question is: if you had to stop working partially or fully, would you be financially ready?

For those relying on employer provided disability insurance, while it’s better than nothing, group policies are full of fine print and limitations (they’re free for a reason). I’ve seen countless cases where employer plans deny or cut off benefits, while private, individual policies continue to pay the claim.

While we can’t control much of our health, we can do our part to be fiscally responsible. And that’s what real financial protection is all about.

Jamie “Elisheva” Kopelman is a disability, life and health insurance broker with National Financial Network in Manhattan. Kopelman is passionate about making financial jargon simple and giving her clients quality insurance protection that fits any budget. She lives in New York City with her family and can be reached at jamie_kopelman@natfin.net or by phone at (631) 560-4701.