Okay, let’s make a quick assessment: Can you afford an extra $117,000 a year? How about $69,000 a year? Or even $48,000 a year?

Chances are that you cannot, certainly not for several consecutive years. If you’re among the lucky ones who could swing it, it would pain you to deplete so much of your assets…especially if you could’ve avoided it.

The above-mentioned expenditures are not far-fetched. They represent the median annual costs New Jersey residents incur for a semi-private nursing home room, residing in an assisted living facility and in-home care, respectively.

Every day, elderly couples—and oftentimes their children—lose their savings and sleep, and go into debt, in order to cope with the physical limitations of aging and/or terminal illness.

You still feel young and energetic, but if you already reached your 40s through 60s, chances are that the physical limitations of aging for you or your spouse are not all that far off anymore. Now is the time to take steps to provide financial security and peace of mind to yourself, your spouse and your offspring.

Welcome to the world of long-term care.

The earlier you get a LTC plan, the better. Not only do you have the peace of mind that you’re covered even if you or your spouse become physically limited before you’d anticipate, Heaven forbid, but it costs you less. At age 40, your LTC premiums will typically be over 35 percent cheaper than at age 50, and over 60 percent cheaper than at age 60.

For example, if a 50-year-old couple is self-insuring their long-term care cost, they will need to put away anywhere from $750,000 to $1,000,000 in liquid assets. A senior couple would pay $17,000 a year for 20 years, which would amount to $340,000 (for $1,000,000 of coverage). So the money that you pay in is less than half of the amount that you would need when self-funding. Saving for premiums to fund a LTC policy is a smarter and more affordable option.

The guidelines of LTC benefits are relatively simple. Once a physician determines that an enrollee can no longer independently perform two of the six “activities of daily living”—eating, bathing, dressing, going to the bathroom, getting in and out of bed or a chair and maintaining continence—you stop paying premiums. You begin receiving benefits that cover 100 percent of the costs of home health aides and therapy, nursing home care, or assisted living facilities—per need.

Some very good news: Married individuals incur lower premiums than singles. Insurance companies are confident that the love and support of your dear spouse will reduce your need for long-term care. They’re right, of course! Insurance companies assume spouses will help each other before hiring an aid, which ultimately saves money. Moreover, benefits can be enjoyed if you live anywhere in the US; this won’t spoil your dream of moving to Florida. If you’re thinking of moving to Israel or another country, many LTC plans can accommodate that too.

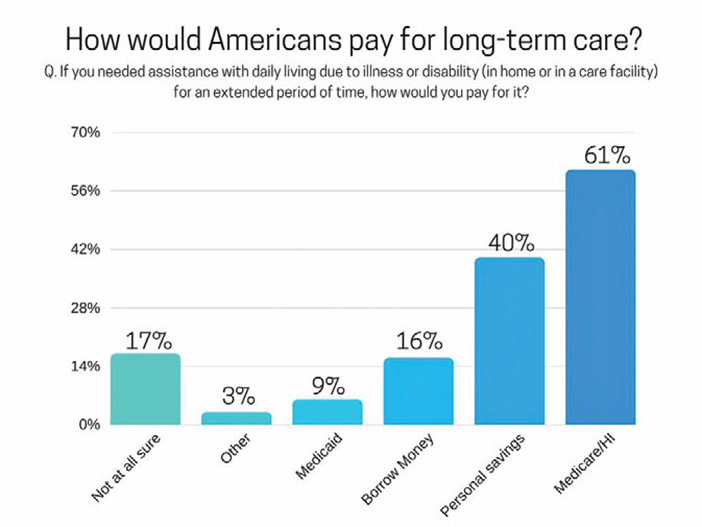

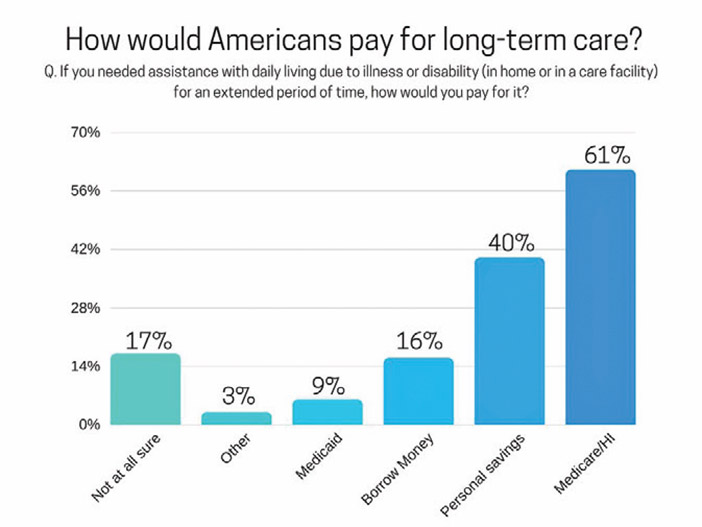

There was a nationwide survey done by OneAmerica that asked Americans, age 45 and older, how they plan to pay for long term care. Over 60 percent of Americans said they plan to pay for long-term care with Medicare or their health insurance. Forty percent of Americans plan to pay for their LTC out of pocket or with their personal savings. Seventeen percent of people said they already had a long-term care insurance plan. A surprising 16 percent said that they would borrow money, from friends, family or spouse. Nine percent would use Medicaid. The remaining 20 percent was not sure at all. Below is a graph to look at to understand the outcome more.

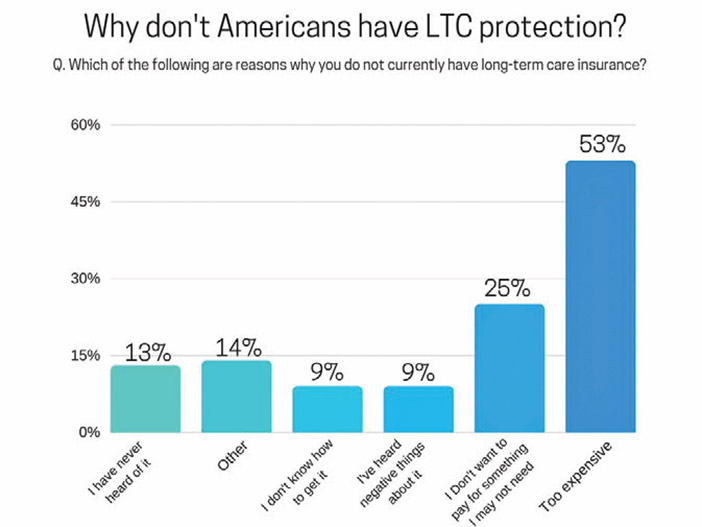

OneAmerica conducted a separate survey asking the same audience, Americans ages 45 and older, why they do not have long-term care protection. The majority of Americans surveyed said that LTC insurance is too expensive. A quarter of the surveyors said they did not want to pay for something they may not need. Eighteen percent of Americans said that they either heard bad things about LTC or they did not know how to purchase it. Thirteen percent had never heard of it and 14 percent gave other reasons.

The following are the primary LTC insurance options available to you today:

Conventional: Conventional LTC insurance works similar to health insurance. As long as you pay a monthly premium, you are covered in the event that you require long term care. When you sign up, the monthly premiums on these policies are lower than the other forms of LTC insurance, but here are the main catches: Premiums are only locked in for one year, and they tend to rise in the subsequent years—sometimes drastically. Also, just as with health and auto insurance, you have little to no benefit from the premiums you paid if you end up needing little or no long-term care in your lifetime.

Life-LTC Hybrid: This is an increasingly popular option that combines the traditional death benefit of life insurance with LTC benefits. You pay a single premium to an insurance carrier that entitles your children to a particular death benefit. If you require long-term care in your lifetime, the insurer will compensate you for the costs tax-free. The amount paid towards this care will be subtracted from the death benefit. Whether or not you will require long-term care, you and/or your children will receive the same total benefits for the premiums you invest. The peace of mind that long-term care expenses will be covered is an inestimable benefit to you and your children.

The cost of hybrid insurance is only nominally higher than for ordinary life insurance, and the premiums are locked in for life. Most people in this age bracket already have conventional life insurance, and we can convert these plans to quality hybrid plans for approximately the same cost they’re already paying. For instance, a 40-year-old couple can get a $325,000 (per spouse) hybrid plan for about $4,000 a year, and a $500,000 (per spouse) benefit for about $6,000 a year. This can be a particularly good choice for people with moderate health issues, because for these plans insurers focus primarily on mortality risk—not risk of requiring long-term care—and the premiums will still be affordable.

The above-mentioned options are the most common options, but not by any mean the only ones. If you don’t believe that any of these are for you, or you’ve been disappointed by the options other agents offered you, don’t despair. We offer a wide variety plans from a wide variety of A+ rated insurers, and we’ll be glad to help you find the best options for your situation. We will be glad to provide you with an option that best suits your needs.

Another important note is that all insurers rate people’s health differently. If an insurer declined you, or gave you an exorbitant premium, due to your health, that doesn’t necessarily mean that you are in bad shape. We can often find an insurer that will rate your health to be satisfactory, even excellent.

Give us a call today! You and your children will be very thankful you did.

Mark Herschlag is the founder and CEO of Cosmo Insurance Agency, which is based in Ocean County. Cosmo Insurance Agency offers personalized solutions for individuals and businesses looking to obtain health, life, dental, long-term care or disability insurance.

For more information or for a free, no-obligation quote, please call (201) 817-1388 or email info@cosmoins.com.

By Mark Herschlag