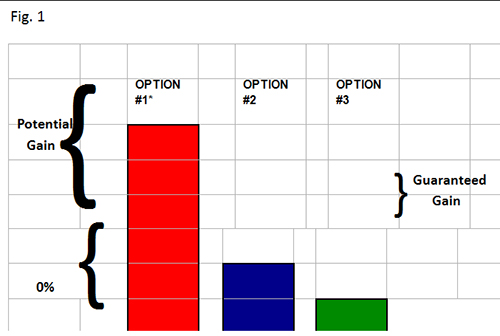

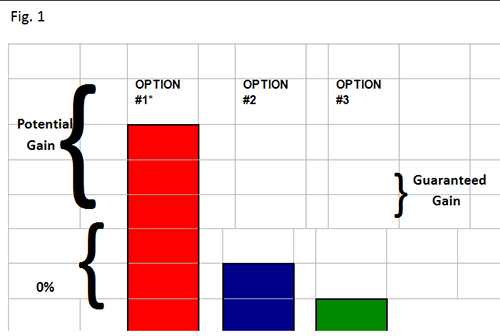

Today’s saver/investor has a vast assortment of financial products for accumulation. However, this array of options can be distilled into three categories. Fig. 1 provides a proportional representation of potential annual returns from these choices. Option 1* products present the greatest opportunity for gain, but also include the risk of loss. Potential returns from Option 2 offerings, while less than Option 1, never incur a loss. Option 3 is a guaranteed return; the upside is limited compared to Options 1 and 2, but an annual increase is assured.

Twenty years ago, most retail investors had only two options, 1 and 3, and allocation strategies consisted of blending market-based (Option 1) and fixed-interest (Option 3) financial products according to one’s objectives and risk tolerance. The range of potential gain and loss might vary depending on the market-based instrument selected, but the proportional spread between the two options remained fairly stable. As investors got older, they typically shifted to fixed products, both to preserve capital and provide an income stream.

However, as annual rates of return on many fixed-interest products have dropped to 1% (or less), many savers find Option 3 instruments unattractive; the return is just too low. Yet the same savers are typically disinclined to add more risk, leaving them to ask, “Isn’t there anything else?”

A response from the financial marketplace has been the introduction of indexed insurance products, primarily annuities. Instead of declaring a guaranteed annual return based on earnings from the insurance company’s investments, the annuity’s crediting rate is tied to the performance of a selected market index, such as the S&P 500 (thus the term “indexed” annuity). If the index shows a gain, the annuity owner receives a percentage of the increase, based on a pre-determined formula. If the index experiences a loss, the annuity owner has no return but preserves principal. This concept is illustrated by Option 2: lower potential positive returns, with a guarantee of no negative returns.

How does this Work? Hedging and Caps

Insurance companies achieve this potential-gain/no-loss result through the use of hedging strategies, “typically in the form of purchasing index call options,” according to Marla G. Lacey, general counsel for a prominent indexed annuity company. If the selected index goes up, the call option gives the insurance company the privilege of “buying the gain.” If the index goes down, the insurance company does not exercise the option; it pays the price of the call, but lets the option expire.

To help fund the no-loss features, the insurance company also imposes a limit on gains. How these “caps” on gains are calculated varies with the annuity contract, but the general effect is that gains from an indexed annuity will be less than gains reported by the index itself. Some examples of these calculations are listed here.

An annual point-to-point crediting formula based on the S&P 500 with a 5% cap means the crediting is based on the difference between the S&P 500 index today and a year from now. If the result is negative, the account value remains the same. If the return is between 0-5%, the account is credited the actual gain. If the gain is more than 5%, the account receives 5%, which is the capped maximum.

Sometimes the cap is expressed as a “participation rate.” An annual point-to-point based on the S&P with a 50% participation rate means the account will receive 50% of any positive returns. If the actual S&P return is 4%, the account receives 2%; if 18%, the account is credited 9%. (But for any negative index results, the annuity owner incurs no losses.)

Consider how these two crediting methods, based on the same index, deliver different results. If the actual S&P return for the policy year was 6%, the first method would credit 5%, while the second would add 3% (50% of 6%). Yet for any return higher than 10%, the second option would credit more to the annuity account.

The determination of caps and crediting calculations for indexed annuities is closely tied to interest rates; higher interest rates will typically result in higher caps, or greater participation rates. Since interest rates are constantly changing, and most indexed annuities are designed to be held for at least five years or longer, many indexed annuity contracts allow the owner to reallocate the account to a different crediting strategy each policy anniversary. A typical indexed annuity may offer five to eight crediting choices, including a guaranteed interest option.

(TO BE CONTINUED…)

*Variable Annuities and their underlying variable investment options are sold by prospectus only. Prospectuses contain important information, including fees and expenses. You should read the prospectus carefully before investing or sending money. Clients should consider the investment objectives, risks, fees and charges of the investment company carefully before investing. The prospectus contains this and other important information. A prospectus may be obtained by contacting your financial professional.

Annuity contracts contain exclusions, limitations, reductions of benefits and terms for keeping them in force. Your licensed financial professional can provide you with complete details.

Variable annuities are long-term investment vehicles that involve certain risks, including possible loss of the principal amount invested. The investment return and principal value may fluctuate so that the investment, when redeemed, may be worth more or less than the original cost. Withdrawals of taxable amounts will be subject to ordinary income tax and possible mandatory federal income tax withholding. If withdrawals are taken prior to age 59?, a 10% IRS penalty may also apply. Withdrawals affect the variable annuity’s death benefit, cash surrender value, and any living benefits and may also be subject to a contingent deferred sales charge.

All guarantees associated with an annuity are backed by the claims-paying ability of the issuing insurance company.

Elozor Preil, RICP®, CLTC is Managing Director at Wealth Advisory Group and Registered Representative and Financial Advisor of Park Avenue Securities LLC (PAS). He can be reached at epreil@wagroupllc.com See www.wagroupllc.com/epreil for full disclosures and disclaimers.

Guardian, its subsidiaries, agents or employees do not give tax or legal advice. You should consult your tax or legal advisor regarding your individual situation.

By Elozor M. Preil