Momentum has picked up and almost every economic indicator is better than it was. People are starting to make more money, and feeling good about the job outlook. The potential to save money has become a reality. Millennials are now going gangbusters in figuring out a way to own a home. The good news is that if you make the jump to homeownership, numerous tax incentives are available, making homeownership even more attractive. Renters should keep in mind that tax incentives can offset the cost of home ownership and significantly reduce their tax liability.

And …. Tax Incentives Here We Go (Remember to Always First Consult With Your Tax Advisor)

1. Interest Deduction on Mortgage Payment

This one tax deduction can add up to a relatively large sum. The amortizations of mortgage loans are typically front loaded with interest payments. Your beginning first payments will have the highest interest-to-principal breakdown, so you get the majority of the tax benefit upfront.

According to the Internal Revenue Service (IRS), “home mortgage interest is any interest you pay on a loan secured by your home (main home or a second home). The loan may be a mortgage to buy your home, a second mortgage, a line of credit, or a home equity loan.”

Fully Deductible Interest

In most cases, you can deduct all of your home mortgage interest. How much you can deduct depends on the date of the mortgage, the amount of the mortgage and how you use the mortgage proceeds.

If all of your mortgages fit into one or more of the following three categories at all times during the year, you can deduct all of the interest on those mortgages. (If any one mortgage fits into more than one category, add the debt that fits in each category to your other debt in the same category.) If one or more of your mortgages does not fit into any of these categories, use Part II of the relevant IRS publication to figure the amount of interest you can deduct.

The three categories are as follows.

1. Mortgages you took out on or before October 13, 1987 (called grandfathered debt).

2. Mortgages you took out after October 13, 1987, to buy, build or improve your home (called home acquisition debt), but only if throughout 2015 these mortgages plus any grandfathered debt totaled $1 million or less ($500,000 or less if married filing separately).

3. Mortgages you took out after October 13, 1987, other than to buy, build or improve your home (called home equity debt), but only if throughout 2015 these mortgages totaled $100,000 or less ($50,000 or less if married filing separately) and totaled no more than the fair market value of your home reduced by (1) and (2).

The dollar limits for the second and third categories apply to the combined mortgages on your main home and second home.

2. Mortgage Credit Certification (MCC)

The Mortgage Credit Certificate (MCC) program provides eligible borrowers a dollar-for-dollar tax credit that lowers the amount of federal taxes they are required to pay to the IRS. An MCC is an on-going federal tax credit that can continue year after year for as long as you retain the loan and occupy the home as your primary residence. Check with your local government housing agency to see if they offer the MCC program to first-time homebuyers in your area.

Amount of the MCC Tax Credit

The amount of the MCC tax credit is based on a percentage of the amount of mortgage interest you pay on the first mortgage loan. The exact percentage of first mortgage interest you can claim is determined by the state, county or city that administers the program for your area.

Here is an example of how the MCC tax credit is calculated assuming the agency administering the MCC program set the percentage at 20 percent, the loan amount is $200,000 and the interest rate is 5 percent:

$200,000 x.05=$10,000 (annual interest)

$10,000 x.20=$2,000 (annual tax credit)

In this example the MCC holder would pay $2,000 less in federal taxes, assuming they had at least $2,000 in total federal tax liability.

To qualify and to claim the MCC tax credit, the borrower or co-borrowers typically must:

· Be a first-time buyer (unless purchasing in a designated target area)

· Meet the applicable income limits adjusted for household size and county

· Purchase an eligible home that meets the purchase price limits

· Purchase a property in the MCC administrator’s program area

· Continue to occupy the home as their primary residence

· Correctly claim the mortgage credit certificate on their federal tax return each tax year

Check with your state or local program administrator for additional program details and requirements

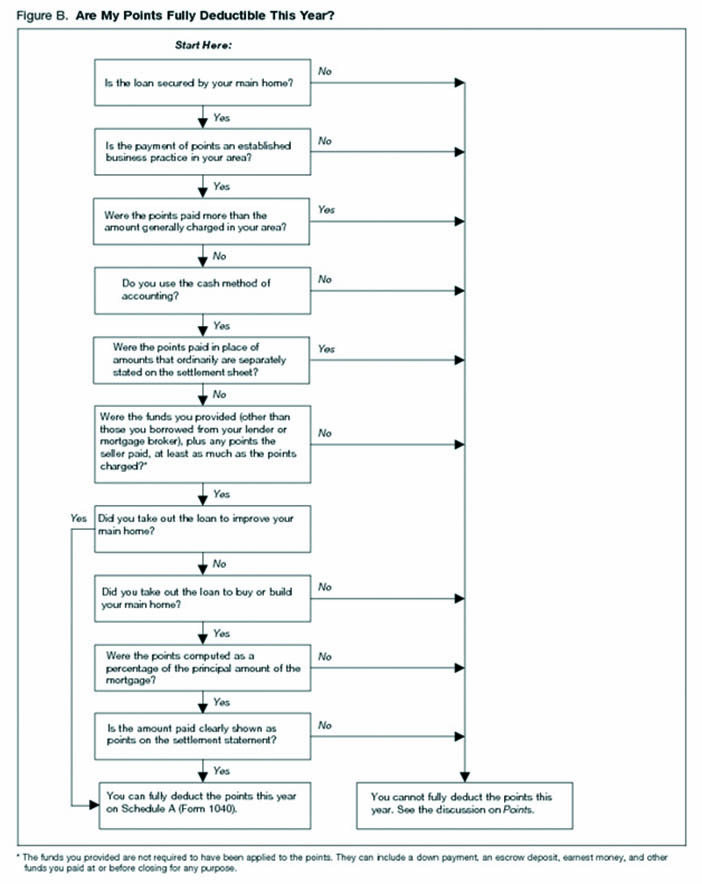

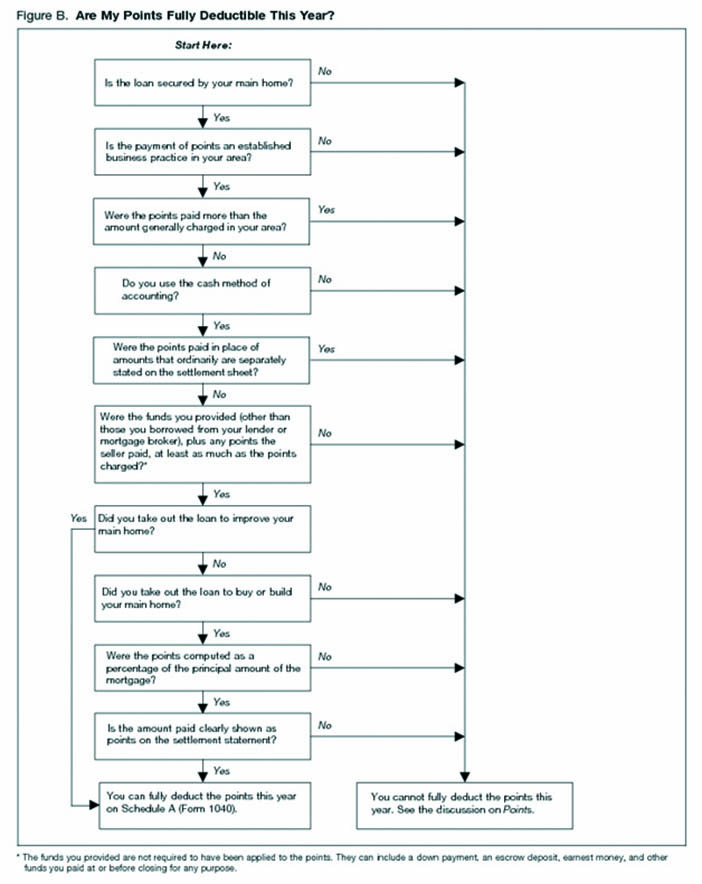

3. Mortgage Origination Fee(s)

(Points)

The term “points” is used to describe “certain charges paid, or treated as paid, by a borrower to obtain a home mortgage. Points may also be called loan origination fees, maximum loan charges, loan discount or discount points. Points are prepaid interest and may be deductible as home mortgage interest, if you itemize deductions.” There are tax guidelines to follow, but in general “If you use a mortgage to buy, build or improve a home you can deduct the interest and points on your mortgage, subject to your mortgage and home equity line not exceeding $1.1 million.” See flow chart, courtesy of the IRS:

4. Tax-Free IRA Withdrawals

A tax-free dip into an IRA for a first-time homebuyer’s down payment is available. The 10 percent penalty normally applied to pre-age 59 1/2 withdrawals is waived. If your current home was not bought in the last two years, you get first-time homebuyer status as well and can take advantage of the free IRA dip for a down payment.

First-time homebuyers are allowed to pull up to $10,000 from their IRA for the purchase of their first home. Married couples can pull up to $20,000. Timing is important, because the funds to purchase a home must be used within 120 days.

If you were on the fence, first-time homebuyers, put the tax incentives in your arsenal of why it may pay to get off the fence and become a homeowner. Call a mortgage professional and your tax advisors, now that tax season is over, and crunch some numbers.

By Carl Guzman

Carl Guzman, NMLS# 65291, CPA, is the founder and President of Greenback Capital Mortgage Corp., a Zillow 5-star lender http://www.zillow.com/profile/Greenback-Capital/Reviews/?my=y. He is a residential and reverse mortgage financing expert and a deal maker with over 26 years’ industry experience. Carl and his team will help you get the best mortgage financing for your situation and his advice will save you thousands! www.greenbackcapital.com, ceg@greenbackcapital.com